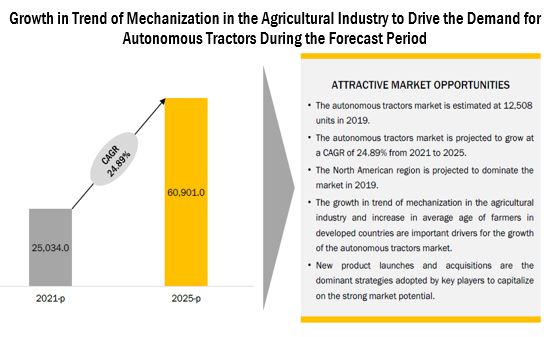

The global autonomous tractors market is projected to witness demand for 12,508 Units in 2019 and 60,901 Units by 2025, at a CAGR of 24.89%. The growth of the market is expected to be driven by the improved efficiency and productivity of crop yield offered by these tractors and growth in initiatives by governments for the adoption of new technologies. The increase in the average age of farmers in developed countries and decline in the availability of labor are also major factors that will drive the demand for autonomous tractors in the near future.

On the basis of power output, 101 HP & above segment will account for the largest share, followed by the 31-100 HP power output segment, in 2019. The demand for medium-powered tractors is expected to grow at a higher rate as compared to high-powered autonomous tractors, owing to the benefits of four-wheeled tractors such as better soil quality maintenance & control, and cultivating capacities with high fuel economy. These tractors are versatile and can be used for multiple applications on and off the field. Owing to these factors, most farmers prefer tractors in this range.

On the basis of component, the radar segment will account for the largest market share in 2019. Radar sensors can determine the velocity, range, and angle of moving objects and can work in almost all weather conditions. They are more cost-effective than LiDAR systems but more expensive compared to cameras.

On the basis of crop type, the fruits & vegetables segment will have the highest application of autonomous tractors. The possibility of machinery damaging fragile fruits & vegetables or the trees that produce them is increasing the demand for new technologies such as autonomous tractors.

The market is dominated by AGCO (US), CNH (UK), Mahindra & Mahindra (India), Deere (US), Kubota Corporation (Japan), Yanmar (Japan), and Autonomous Tractor Corporation (US).These companies have a strong distribution network at the global level. The key strategies adopted by these companies to sustain their market position are new product development and acquisitions. All the parameters mentioned above have been analyzed to derive the market ranking of these companies.